Portfolio Update: 1.23.20

The ALL-NEW 2020 Daily Decision Model Portfolio

NEW TRADING STRATEGY FOR 2020!

About The Portfolio: The Daily Decision Model Portfolio is an aggressive, actively risk-managed, multi-strategy, multi-manager approach. The primary objective of the portfolio is to stay in tune with the major market cycles - both bull and bear. However, the portfolio will, at times, actively manage exposures based on shorter-term moves. In addition to "timing" moves, the portfolio will utilize levered positions via ETFs and may hold an effective net short position during negative cycles.

Strategy Diversification: The 2020 DD Portfolio utilizes a well diversified approach. The management strategy incorporates multiple trading strategies so as to avoid the "singular failure" problem that can occur when a single strategy is out of sync. There are a total of 9 different trading strategies working in the 2020 DD Portfolio. Three "turbo-charged" aggressive beta strategies. Three mean reversion strategies. And three risk-management strategies. In addition, there are three separate managers working in the portfolio.

An Actively Traded Approach: We anticipate the portfolio will trade 2-3 times a week and hold between two and four ETF positions. Finally, please note that the Daily Decision Portfolio strategy is aggressive in nature and thus, drawdowns can and will occur. However, we believe the strategy will rebound quickly after temporary pullbacks.

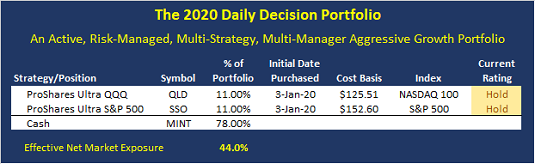

Current Positions

Below are the current positions for the 2020 Daily Decision Model Portfolio.

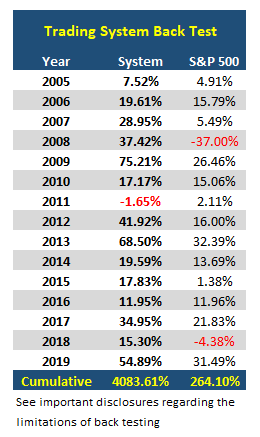

Testing The Trading Systems

In our humble opinion, it would be foolish to utilize any trading approach without first testing the strategy. However, when you combine strategies that have never been combined before, you have a hypothetical strategy. As such, you must do a back test on the combination.

There is a well known saying in the investment management business relating to hypothetical tests of trading systems that goes a little something like this: "Back tests are bull*#$!"

To be sure, there are problems involved with back testing, not the least of which is curve fitting. I.E. making your system fit the data provided. This is what happens when inexperienced traders try to develop systems that would have done well historically.

However, our approach here is different. We aren't using back testing to develop strategies to trade the market. No, we are testing a combination of EXISTING systems in effort to create "proof of concept." In other words, does a certain combination of systems developed by different managers work well together over time?

Wishing You All The Best in Your Investing Endeavors!

The Front Range Trading Team

NOT INVESTMENT ADVICE. The analysis and information in this report and on our website is for informational purposes only. No part of the material presented in this report or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any Portfolio constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the editors and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Position Disclosure:At the time of publication, the editors hold long positions in the following securities mentioned: SSO, QLD - Note that positions may change at any time.

Important Disclosures Relating to the Limitations of Back Testing:

The preceding summary of hypothetical performance is for illustrative purposes only and is not a solicitation or recommendation of any investment strategy.

There is no guarantee that investment results portrayed in this illustration will yield similar future results. All investments and/or investment strategies involve risk including the possible loss of principal. Consult an investment professional before investing in any investment program.

In the illustration we have utilized hypothetical back testing to create the performance record to reflect the manner in which an account could be managed. Hypothetical back tested performance results have many inherent limitations and do not reflect the actual results of any client account.

Hypothetical performance results are achieved by means of the retroactive mixing of portfolio strategies that was designed and prepared with the benefit of hindsight. No representation is being made that any strategy will or is likely to achieve profits or have losses similar to those shown. Hypothetical testing may not reflect the impact that any material market or economic factor may have on investment decision making. Further, the performance record in this illustration may have under or over compensated for the impact, if any, of certain market factors (e.g. lack of liquidity, trading costs, etc.). The conditions, objectives or investment strategies may have changed materially during the time period, or after the time period, portrayed in this performance record, and the effect of such change is not portrayed in the performance record.

Hypothetical back tested performance results are shown gross of management fees. Hypothetical back tested performance results are before trading and other custodian costs and do not consider the impact of taxes.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS